Insurance Blog

Disclaimer

The views, information, and comments in this blog should be understood as the personal opinions of the author and provide only a simplified description of coverages and is not a statement of contract. Insurance products and coverages may not apply in all states.

2025 ACA & Medicaid Changes: What You Need to Know

Sunday, July 6, 2025 1 Stop Benefits, Inc.

Big changes to health insurance rules are here-and many people could lose coverage if they don't act. We're here to make sure that's not you.

No More Auto-Renewals

What this means:

If you have an ACA Marketplace plan, you'll now need to re-apply every year. No more automatic re-enrollment.

What to do:

Big changes to health insurance rules are here-and many people could lose coverage if they don't act. We're here to make sure that's not you.

No More Auto-Renewals

What this means:

If you have an ACA Marketplace plan, you'll now need to re-apply every year. No more automatic re-enrollment.

What to do:

Big changes to health insurance rules are here-and many people could lose coverage if they don't act. We're here to make sure that's not you.

No More Auto-Renewals

What this means:

If you have an ACA Marketplace plan, you'll now need to re-apply every year. No more automatic re-enrollment.

What to do:

- Mark your calendar for the shorter Open Enrollment period.

- Work with us early-we'll make sure your application is submitted on time and with all documentation.

- Be ready to show pay stubs, tax info, or other documents during the year.

- Let us help with gathering and uploading your documents.

- Let us shop all available options-Marketplace, off-Marketplace, short-term, or employer alternatives.

- Ask about bundling dental, vision, or enhanced life and long-term care benefits.

- Check if you qualify for an exemption (health, caregiving, student status).

- We'll help track and report work hours or file exemption paperwork.

- We can explore affordable private options that don't rely on ACA subsidies.

- Ask us about guaranteed issue and low-premium limited benefit plans.

Part-Time Surveys, Full-Time Health Benefits: A Smarter Way to Get Covered

Wednesday, April 10, 2025 Craig Chapin

In today's evolving healthcare environment, innovative programs are reshaping how individuals access meaningful, affordable coverage. LifeX and Population Science Management (PSM) are leading the charge by offering a unique model: contribute to public health research through short, part-time surveys-and in return, gain access to comprehensive group health insurance.

How It Works

Both companies hire individuals as part-time associates to complete occasional surveys- each typically taking just 5 to 10 minutes, with only a few hours required over the course of a year. Participants are paid for their time and, more importantly, gain access to high-quality, off-exchange health insurance plans.

At 1 Stop Benefits, Inc., we're proud to serve as a recruiting partner for these programs, connecting individuals with this smart, impactful opportunity. It's a win-win: contribute to better public health while securing valuable coverage for yourself and your family.

Highlights of Off-Exchange Group Health Plans

Ready to learn more or see if you qualify? Reach out to 1 Stop Benefits today-we're happy to walk you through your options and answer any questions, with no pressure. Call us at 1-800-662-3982 or email: info@1StopBenefits.com to get started.

In today's evolving healthcare environment, innovative programs are reshaping how individuals access meaningful, affordable coverage. LifeX and Population Science Management (PSM) are leading the charge by offering a unique model: contribute to public health research through short, part-time surveys-and in return, gain access to comprehensive group health insurance.

How It Works

Both companies hire individuals as part-time associates to complete occasional surveys- each typically taking just 5 to 10 minutes, with only a few hours required over the course of a year. Participants are paid for their time and, more importantly, gain access to high-quality, off-exchange health insurance plans.

At 1 Stop Benefits, Inc., we're proud to serve as a recruiting partner for these programs, connecting individuals with this smart, impactful opportunity. It's a win-win: contribute to better public health while securing valuable coverage for yourself and your family.Highlights of Off-Exchange Group Health Plans

- Flexible Plan Options -- Choose from a range of deductibles and coverage levels

- Great for High Earners -- Ideal for those ineligible for ACA subsidies

- Eligibility -- Available to 1099 contractors, self-employed professionals, and non-working individuals under age 65

By classifying survey participants as part-time associates, LifeX and PSM can offer group health plans-making comprehensive insurance accessible to more people, especially those who fall through the cracks of traditional systems.

- No Balance Billing -- Pre-negotiated rates help reduce unexpected costs

- Lower Shared Expenses -- In-network care keeps your out-of-pocket costs down

- Comprehensive Benefits -- Includes telehealth, pharmacy coverage, and chronic care support

- Freedom of Access -- Nationwide networks with no referrals required

- LifeX -- Tiered premiums with access to PHCS, Cigna, and Anthem

- PSM -- Nationwide access via Blue Cross Blue Shield and PHCS

- Health Surveys + EHRs -- Combine insights for a full picture of health trends

- Predictive Analytics -- Identify emerging risks and support early intervention

- Personalized Solutions -- Tailor strategies to improve community health outcomes

Ready to learn more or see if you qualify? Reach out to 1 Stop Benefits today-we're happy to walk you through your options and answer any questions, with no pressure. Call us at 1-800-662-3982 or email: info@1StopBenefits.com to get started.

Two Plans Are Better Than One

Monday, August 21, 2023 Craig E Chapin

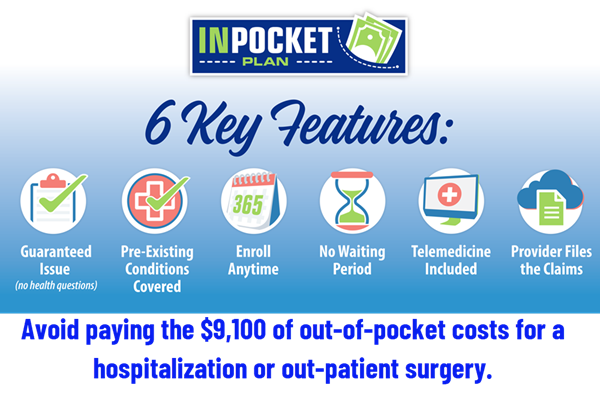

In an ever-changing healthcare landscape, arming yourself with knowledge about health insurance is vital not only for your physical health but also for your financial security. A new insurance plan offers relief to individuals covered by Affordable Care individual health plans regardless of medical conditions and without the standard exclusions. Now, having two insurance plans provides lower out-of-pocket costs than one. The MOOP (maximum out-of-pocket) expenses will be $9,200 per individual and $18,400 per family 2025. Tiered health plans can speed up your obligations. Start saving or read on.

In the insurance industry, one thing remains consistent. 20% of people use 80% of healthcare expenses. Since the Obama Care began, individuals have been insured regardless of their pre-existing conditions or medical expenses. Premium costs have been increasing every year since the law was passed. However, for many participants, the actual premium cost is not obvious as the subsidies granted by the Affordable Care Act offset the increases. What is apparent is that the out-of-pocket costs are increasing and are unaffordable for the average family.

For many, hospital indemnity insurance plans fill the gap for a fraction of the cost of buying up to gold health plans. However, not all states allow hospital indemnity plans to be offered to individuals. Most do not cover the significant upfront costs on the first day in the hospital, and few cover outpatient surgeries. Most are also unavailable to people with pre-existing conditions, and just about all do not cover maternity and mental health expenses.

Life happens, and everyone needs to set up an emergency fund or leverage their limited funds. Solutions now exist to cover your medical bills for accidents only or both sickness and accidents. Do the math to save money by comparing the MOOP and premiums on bronze, silver, and gold individual health plans. People covered by tiered networks (i.e., Proactive Plans) must understand that an ambulance takes you to the nearest hospital regardless of tier status or network. (St Mary's is Tier 3 with Keystone Proactive Plans). Consider lowering your out-of-pocket costs for families planning on more children or baby boomers with a higher risk of hospitalization. Sleep better knowing you can afford to be taken to the nearest hospital or get treated without the risk of medical bankruptcy.

In an ever-changing healthcare landscape, arming yourself with knowledge about health insurance is vital not only for your physical health but also for your financial security. A new insurance plan offers relief to individuals covered by Affordable Care individual health plans regardless of medical conditions and without the standard exclusions. Now, having two insurance plans provides lower out-of-pocket costs than one. The MOOP (maximum out-of-pocket) expenses will be $9,200 per individual and $18,400 per family 2025. Tiered health plans can speed up your obligations. Start saving or read on.

In the insurance industry, one thing remains consistent. 20% of people use 80% of healthcare expenses. Since the Obama Care began, individuals have been insured regardless of their pre-existing conditions or medical expenses. Premium costs have been increasing every year since the law was passed. However, for many participants, the actual premium cost is not obvious as the subsidies granted by the Affordable Care Act offset the increases. What is apparent is that the out-of-pocket costs are increasing and are unaffordable for the average family.

For many, hospital indemnity insurance plans fill the gap for a fraction of the cost of buying up to gold health plans. However, not all states allow hospital indemnity plans to be offered to individuals. Most do not cover the significant upfront costs on the first day in the hospital, and few cover outpatient surgeries. Most are also unavailable to people with pre-existing conditions, and just about all do not cover maternity and mental health expenses.

Life happens, and everyone needs to set up an emergency fund or leverage their limited funds. Solutions now exist to cover your medical bills for accidents only or both sickness and accidents. Do the math to save money by comparing the MOOP and premiums on bronze, silver, and gold individual health plans. People covered by tiered networks (i.e., Proactive Plans) must understand that an ambulance takes you to the nearest hospital regardless of tier status or network. (St Mary's is Tier 3 with Keystone Proactive Plans). Consider lowering your out-of-pocket costs for families planning on more children or baby boomers with a higher risk of hospitalization. Sleep better knowing you can afford to be taken to the nearest hospital or get treated without the risk of medical bankruptcy.

In an ever-changing healthcare landscape, arming yourself with knowledge about health insurance is vital not only for your physical health but also for your financial security. A new insurance plan offers relief to individuals covered by Affordable Care individual health plans regardless of medical conditions and without the standard exclusions. Now, having two insurance plans provides lower out-of-pocket costs than one. The MOOP (maximum out-of-pocket) expenses will be $9,200 per individual and $18,400 per family 2025. Tiered health plans can speed up your obligations. Start saving or read on.

In the insurance industry, one thing remains consistent. 20% of people use 80% of healthcare expenses. Since the Obama Care began, individuals have been insured regardless of their pre-existing conditions or medical expenses. Premium costs have been increasing every year since the law was passed. However, for many participants, the actual premium cost is not obvious as the subsidies granted by the Affordable Care Act offset the increases. What is apparent is that the out-of-pocket costs are increasing and are unaffordable for the average family.

For many, hospital indemnity insurance plans fill the gap for a fraction of the cost of buying up to gold health plans. However, not all states allow hospital indemnity plans to be offered to individuals. Most do not cover the significant upfront costs on the first day in the hospital, and few cover outpatient surgeries. Most are also unavailable to people with pre-existing conditions, and just about all do not cover maternity and mental health expenses.

Life happens, and everyone needs to set up an emergency fund or leverage their limited funds. Solutions now exist to cover your medical bills for accidents only or both sickness and accidents. Do the math to save money by comparing the MOOP and premiums on bronze, silver, and gold individual health plans. People covered by tiered networks (i.e., Proactive Plans) must understand that an ambulance takes you to the nearest hospital regardless of tier status or network. (St Mary's is Tier 3 with Keystone Proactive Plans). Consider lowering your out-of-pocket costs for families planning on more children or baby boomers with a higher risk of hospitalization. Sleep better knowing you can afford to be taken to the nearest hospital or get treated without the risk of medical bankruptcy.

Updates to Medicare Part D Medication Coverage

Tuesday, July 18, 2023 Craig E Chapin

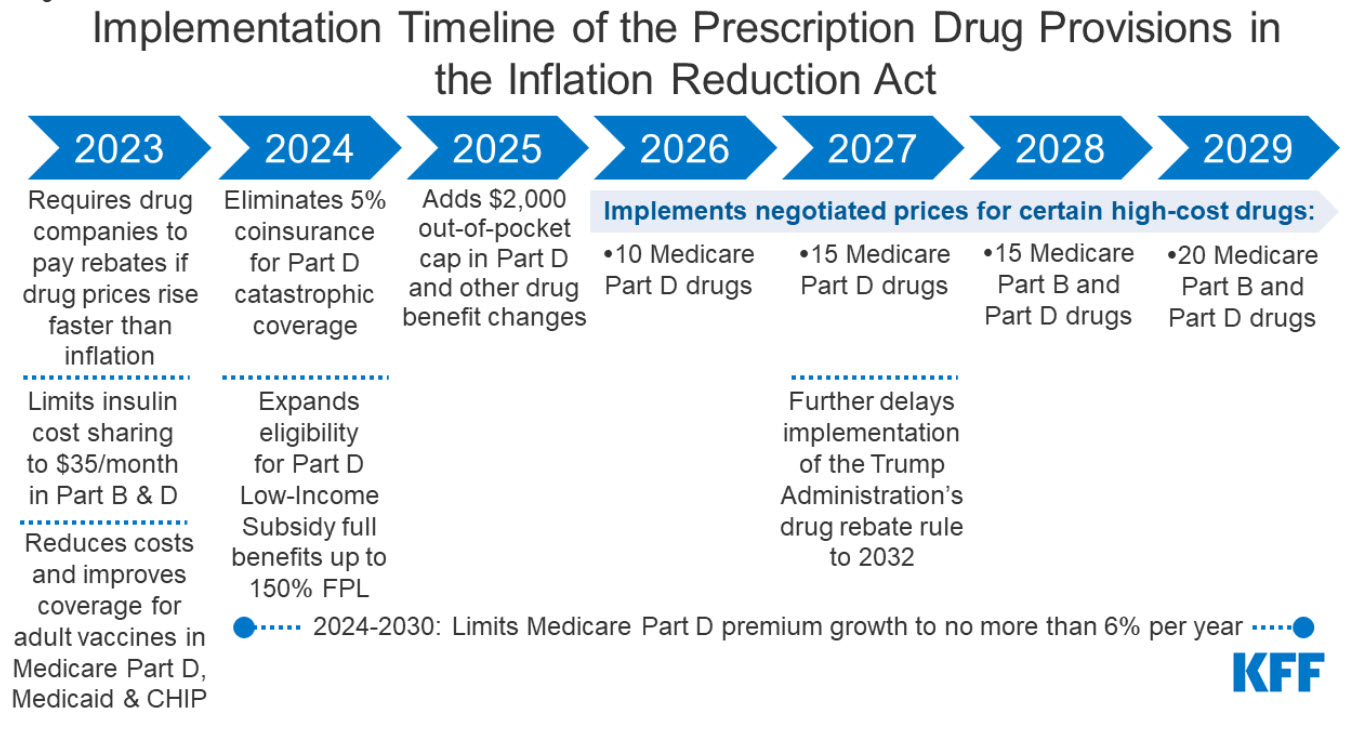

Staying informed about changes to Medicare Part D medication coverage is essential for understanding how these updates may impact healthcare expenses and treatment options. This blog post will explore the recent Medicare Part D medication coverage improvements that the Infl initiated by the Inflation Reduction Act.

1. The law requires the federal government to negotiate prices for some high-cost drugs covered under Medicare. Medicare Part D and Part B drug spending are highly concentrated among a relatively small share of covered drugs, mainly those without generic or biosimilar competitors. Under the Inflation Reduction Act, brand-name and biologic drugs without generic or biosimilar equivalents covered under Medicare Part D that are among the highest-spending Medicare-covered drugs are eligible for negotiation. The number of negotiated drugs is limited to 10 Part D drugs in 2026, another 15 Part D drugs in 2027, another 15 Part B and Part D drugs in 2028, and another 20 Part B and Part D drugs in 2029 and later years.

2. The law requires drug manufacturers to pay Medicare rebates if they increase prices faster than inflation for drugs used by Medicare beneficiaries. The inflation rebate provision will be implemented in 2023, using 2021 as the base year for determining price changes relative to inflation.

3. The law Caps Medicare beneficiaries' out-of-pocket spending under the Medicare Part D benefit, first eliminating coinsurance above the catastrophic threshold in 2024 and then adding a $2,000 cap on spending in 2025. It also limits annual increases in Part D premiums from 2024 to 2030 and makes other changes to the Part D benefit design.

4. Beginning in 2023, the bill limits cost-sharing for insulin to $35 per month for people with Medicare, including covered insulin products in Medicare Part D plans, beginning January 1, 2023, and for insulin furnished through durable medical equipment under Medicare Part B, starting July 1, 2023.

5. Eliminates cost-sharing for adult vaccines covered under Medicare Part D, as of 2023, and improves access to adult vaccines under Medicaid and CHIP.

6. It expands eligibility for full Part D Low-Income Subsidies (LIS) in 2024 to low-income beneficiaries with incomes up to 150% of poverty and modest assets and repeals the partial LIS benefit currently in place for individuals with incomes between 135% and 150% of poverty.

7. Expanded Medication Therapy Management (MTM) Services: MTM services have been expanded to provide enhanced support and guidance. This helps ensure effective medication use, improves health outcomes, and minimizes drug-related issues.

8. Enhanced Information and Decision-Making Tools: Beneficiaries now have improved resources for informed decision-making. The updated Plan Finder tool offers accurate cost estimates and helps select the most suitable Part D plan based on individual medication needs.

Conclusion: Staying updated on Medicare Part D medication coverage changes is crucial for beneficiaries seeking affordable and necessary prescription drugs. Recent enhancements, including improved coverage in the donut hole, biosimilar discounts, expanded catastrophic coverage threshold, expanded MTM services, and enhanced information tools, contribute to greater affordability and accessibility. Beneficiaries are encouraged to remain informed, review their Part D plan regularly, and utilize available resources to make informed decisions about prescription drug coverage.

Disclaimer: The information provided is for educational purposes only and not legal or financial advice. Consult a qualified professional for personalized guidance regarding your specific situation.

Staying informed about changes to Medicare Part D medication coverage is essential for understanding how these updates may impact healthcare expenses and treatment options. This blog post will explore the recent Medicare Part D medication coverage improvements that the Infl initiated by the Inflation Reduction Act.

1. The law requires the federal government to negotiate prices for some high-cost drugs covered under Medicare. Medicare Part D and Part B drug spending are highly concentrated among a relatively small share of covered drugs, mainly those without generic or biosimilar competitors. Under the Inflation Reduction Act, brand-name and biologic drugs without generic or biosimilar equivalents covered under Medicare Part D that are among the highest-spending Medicare-covered drugs are eligible for negotiation. The number of negotiated drugs is limited to 10 Part D drugs in 2026, another 15 Part D drugs in 2027, another 15 Part B and Part D drugs in 2028, and another 20 Part B and Part D drugs in 2029 and later years.

2. The law requires drug manufacturers to pay Medicare rebates if they increase prices faster than inflation for drugs used by Medicare beneficiaries. The inflation rebate provision will be implemented in 2023, using 2021 as the base year for determining price changes relative to inflation.

3. The law Caps Medicare beneficiaries' out-of-pocket spending under the Medicare Part D benefit, first eliminating coinsurance above the catastrophic threshold in 2024 and then adding a $2,000 cap on spending in 2025. It also limits annual increases in Part D premiums from 2024 to 2030 and makes other changes to the Part D benefit design.

4. Beginning in 2023, the bill limits cost-sharing for insulin to $35 per month for people with Medicare, including covered insulin products in Medicare Part D plans, beginning January 1, 2023, and for insulin furnished through durable medical equipment under Medicare Part B, starting July 1, 2023.

5. Eliminates cost-sharing for adult vaccines covered under Medicare Part D, as of 2023, and improves access to adult vaccines under Medicaid and CHIP.

6. It expands eligibility for full Part D Low-Income Subsidies (LIS) in 2024 to low-income beneficiaries with incomes up to 150% of poverty and modest assets and repeals the partial LIS benefit currently in place for individuals with incomes between 135% and 150% of poverty.

7. Expanded Medication Therapy Management (MTM) Services: MTM services have been expanded to provide enhanced support and guidance. This helps ensure effective medication use, improves health outcomes, and minimizes drug-related issues.

8. Enhanced Information and Decision-Making Tools: Beneficiaries now have improved resources for informed decision-making. The updated Plan Finder tool offers accurate cost estimates and helps select the most suitable Part D plan based on individual medication needs.

Conclusion: Staying updated on Medicare Part D medication coverage changes is crucial for beneficiaries seeking affordable and necessary prescription drugs. Recent enhancements, including improved coverage in the donut hole, biosimilar discounts, expanded catastrophic coverage threshold, expanded MTM services, and enhanced information tools, contribute to greater affordability and accessibility. Beneficiaries are encouraged to remain informed, review their Part D plan regularly, and utilize available resources to make informed decisions about prescription drug coverage.

Disclaimer: The information provided is for educational purposes only and not legal or financial advice. Consult a qualified professional for personalized guidance regarding your specific situation.

Staying informed about changes to Medicare Part D medication coverage is essential for understanding how these updates may impact healthcare expenses and treatment options. This blog post will explore the recent Medicare Part D medication coverage improvements that the Infl initiated by the Inflation Reduction Act.

1. The law requires the federal government to negotiate prices for some high-cost drugs covered under Medicare. Medicare Part D and Part B drug spending are highly concentrated among a relatively small share of covered drugs, mainly those without generic or biosimilar competitors. Under the Inflation Reduction Act, brand-name and biologic drugs without generic or biosimilar equivalents covered under Medicare Part D that are among the highest-spending Medicare-covered drugs are eligible for negotiation. The number of negotiated drugs is limited to 10 Part D drugs in 2026, another 15 Part D drugs in 2027, another 15 Part B and Part D drugs in 2028, and another 20 Part B and Part D drugs in 2029 and later years.

2. The law requires drug manufacturers to pay Medicare rebates if they increase prices faster than inflation for drugs used by Medicare beneficiaries. The inflation rebate provision will be implemented in 2023, using 2021 as the base year for determining price changes relative to inflation.

3. The law Caps Medicare beneficiaries' out-of-pocket spending under the Medicare Part D benefit, first eliminating coinsurance above the catastrophic threshold in 2024 and then adding a $2,000 cap on spending in 2025. It also limits annual increases in Part D premiums from 2024 to 2030 and makes other changes to the Part D benefit design.

4. Beginning in 2023, the bill limits cost-sharing for insulin to $35 per month for people with Medicare, including covered insulin products in Medicare Part D plans, beginning January 1, 2023, and for insulin furnished through durable medical equipment under Medicare Part B, starting July 1, 2023.

5. Eliminates cost-sharing for adult vaccines covered under Medicare Part D, as of 2023, and improves access to adult vaccines under Medicaid and CHIP.

6. It expands eligibility for full Part D Low-Income Subsidies (LIS) in 2024 to low-income beneficiaries with incomes up to 150% of poverty and modest assets and repeals the partial LIS benefit currently in place for individuals with incomes between 135% and 150% of poverty.

7. Expanded Medication Therapy Management (MTM) Services: MTM services have been expanded to provide enhanced support and guidance. This helps ensure effective medication use, improves health outcomes, and minimizes drug-related issues.

8. Enhanced Information and Decision-Making Tools: Beneficiaries now have improved resources for informed decision-making. The updated Plan Finder tool offers accurate cost estimates and helps select the most suitable Part D plan based on individual medication needs.

Conclusion: Staying updated on Medicare Part D medication coverage changes is crucial for beneficiaries seeking affordable and necessary prescription drugs. Recent enhancements, including improved coverage in the donut hole, biosimilar discounts, expanded catastrophic coverage threshold, expanded MTM services, and enhanced information tools, contribute to greater affordability and accessibility. Beneficiaries are encouraged to remain informed, review their Part D plan regularly, and utilize available resources to make informed decisions about prescription drug coverage.

Disclaimer: The information provided is for educational purposes only and not legal or financial advice. Consult a qualified professional for personalized guidance regarding your specific situation.

NJ is making a mistake by robbing the group health market to pay for the NJHPTC.

Thursday, March 24, 2023 Craig E Chapin, Pesident

Using NJ state and federal subsidies, the Affordable Care Act (ACA) helps eligible individuals and families afford health insurance. The American Rescue Plan Act has increased the amount of financial help available, with no one paying more than 8.5% of their income for health insurance when not offered affordable group health insurance through work. New Jersey has its own subsidy program, the New Jersey Health Insurance Premium Tax Credit (NJHPTC), funded by state taxes, fees, and assessments on health insurance companies and hospitals, as well as the state's general fund. However, NJ added subsidy may cause small employers to stop offering group health plans.

To be eligible for NJHPTC, individuals, and families must meet certain income requirements, and the amount of subsidy varies based on the number of insured individuals. For example, an individual making 150% of the Federal Poverty Level will receive combined subsidies, making many health plans have zero premiums. Adults making less than 401% of the FPL get an extra $100 a month, and incomes between 401% to 600% of the FPL will get $50 a month.

Children dependents under age 19 default to the Children's Health Insurance Program at zero cost if the household earns less than 355% of the FPL. The adults receive the NJHPTC as indicated above. If the child is over 18, they are treated as an adult, getting up to an additional $100 credit per child under 400% of the FPL and $50 from 401% up to 600% of the FPL.

The CHIP insures over one million children in NJ, and growing the pool is a priority to move to a one-payer system. To avoid a child's eligibility for CHIP, the family must report an income over 355% of the FPL, or they can refuse the free coverage and enroll their children in a non-subsidized plan through the same insurance companies offered to adults. The Child Health Insurance Program offers comprehensive coverage, including dental and vision.

When a state takes funds from the health industry and hospitals to fund the subsidy, insurance companies and hospitals will pass the cost on to all users, increasing the overall cost. Eventually, as small group premiums increase, many employers will stop offering group coverage and direct employees to purchase subsidized individual plans. The Family Glitch Fix will further enlighten employers about how little individuals pay for health insurance. The fix allows dependents of employees covered by group health plans to enroll in subsidized individual health plans if the household cost is determined unaffordable. Groups under 50 employees do not have a penalty for not offering health insurance, so when the cost can be sliced in half, an employer's premium contributions may be better allocated to other benefits or an increase in pay.

The subsidy programs aim to balance the cost burden across different groups, with the hope that increased access to healthcare will ultimately lead to better health outcomes and lower overall healthcare costs in the long run. With over forty years of experience, I feel usage will increase, moral hazard will not lead to better healthcare outcomes, and participants will demand the entitlement to be maintained while others pay the cost.

Using NJ state and federal subsidies, the Affordable Care Act (ACA) helps eligible individuals and families afford health insurance. The American Rescue Plan Act has increased the amount of financial help available, with no one paying more than 8.5% of their income for health insurance when not offered affordable group health insurance through work. New Jersey has its own subsidy program, the New Jersey Health Insurance Premium Tax Credit (NJHPTC), funded by state taxes, fees, and assessments on health insurance companies and hospitals, as well as the state's general fund. However, NJ added subsidy may cause small employers to stop offering group health plans.

To be eligible for NJHPTC, individuals, and families must meet certain income requirements, and the amount of subsidy varies based on the number of insured individuals. For example, an individual making 150% of the Federal Poverty Level will receive combined subsidies, making many health plans have zero premiums. Adults making less than 401% of the FPL get an extra $100 a month, and incomes between 401% to 600% of the FPL will get $50 a month.

Children dependents under age 19 default to the Children's Health Insurance Program at zero cost if the household earns less than 355% of the FPL. The adults receive the NJHPTC as indicated above. If the child is over 18, they are treated as an adult, getting up to an additional $100 credit per child under 400% of the FPL and $50 from 401% up to 600% of the FPL.

The CHIP insures over one million children in NJ, and growing the pool is a priority to move to a one-payer system. To avoid a child's eligibility for CHIP, the family must report an income over 355% of the FPL, or they can refuse the free coverage and enroll their children in a non-subsidized plan through the same insurance companies offered to adults. The Child Health Insurance Program offers comprehensive coverage, including dental and vision.

When a state takes funds from the health industry and hospitals to fund the subsidy, insurance companies and hospitals will pass the cost on to all users, increasing the overall cost. Eventually, as small group premiums increase, many employers will stop offering group coverage and direct employees to purchase subsidized individual plans. The Family Glitch Fix will further enlighten employers about how little individuals pay for health insurance. The fix allows dependents of employees covered by group health plans to enroll in subsidized individual health plans if the household cost is determined unaffordable. Groups under 50 employees do not have a penalty for not offering health insurance, so when the cost can be sliced in half, an employer's premium contributions may be better allocated to other benefits or an increase in pay.

The subsidy programs aim to balance the cost burden across different groups, with the hope that increased access to healthcare will ultimately lead to better health outcomes and lower overall healthcare costs in the long run. With over forty years of experience, I feel usage will increase, moral hazard will not lead to better healthcare outcomes, and participants will demand the entitlement to be maintained while others pay the cost.

Using NJ state and federal subsidies, the Affordable Care Act (ACA) helps eligible individuals and families afford health insurance. The American Rescue Plan Act has increased the amount of financial help available, with no one paying more than 8.5% of their income for health insurance when not offered affordable group health insurance through work. New Jersey has its own subsidy program, the New Jersey Health Insurance Premium Tax Credit (NJHPTC), funded by state taxes, fees, and assessments on health insurance companies and hospitals, as well as the state's general fund. However, NJ added subsidy may cause small employers to stop offering group health plans.

To be eligible for NJHPTC, individuals, and families must meet certain income requirements, and the amount of subsidy varies based on the number of insured individuals. For example, an individual making 150% of the Federal Poverty Level will receive combined subsidies, making many health plans have zero premiums. Adults making less than 401% of the FPL get an extra $100 a month, and incomes between 401% to 600% of the FPL will get $50 a month.

Children dependents under age 19 default to the Children's Health Insurance Program at zero cost if the household earns less than 355% of the FPL. The adults receive the NJHPTC as indicated above. If the child is over 18, they are treated as an adult, getting up to an additional $100 credit per child under 400% of the FPL and $50 from 401% up to 600% of the FPL.

The CHIP insures over one million children in NJ, and growing the pool is a priority to move to a one-payer system. To avoid a child's eligibility for CHIP, the family must report an income over 355% of the FPL, or they can refuse the free coverage and enroll their children in a non-subsidized plan through the same insurance companies offered to adults. The Child Health Insurance Program offers comprehensive coverage, including dental and vision.

When a state takes funds from the health industry and hospitals to fund the subsidy, insurance companies and hospitals will pass the cost on to all users, increasing the overall cost. Eventually, as small group premiums increase, many employers will stop offering group coverage and direct employees to purchase subsidized individual plans. The Family Glitch Fix will further enlighten employers about how little individuals pay for health insurance. The fix allows dependents of employees covered by group health plans to enroll in subsidized individual health plans if the household cost is determined unaffordable. Groups under 50 employees do not have a penalty for not offering health insurance, so when the cost can be sliced in half, an employer's premium contributions may be better allocated to other benefits or an increase in pay.

The subsidy programs aim to balance the cost burden across different groups, with the hope that increased access to healthcare will ultimately lead to better health outcomes and lower overall healthcare costs in the long run. With over forty years of experience, I feel usage will increase, moral hazard will not lead to better healthcare outcomes, and participants will demand the entitlement to be maintained while others pay the cost.

All employees with dependents need to see if the "Family Glitch Fix" applies to them.

Thursday, March 16, 2023

The "Family Glitch Fix" allows employees with dependent group health coverage to save thousands. Once notified, the fix allows employee dependents denied access to subsidized individual health plans to enroll immediately.

Call us, and we can check affordability in seconds, then calculate your monthly savings in any health plan offered in your area. If your employer offers group health insurance and you have dependents, you may be able to lower your premium costs and their out-of-pocket costs for medical care.

The so-called "family glitch" stems from a 2013 IRS interpretation. Under Section 36B of the Internal Revenue Code, individuals generally do not qualify for premium tax credits if they are eligible for another source of minimum essential coverage, including employer-sponsored plans. There are two exceptions to this rule under the ACA-when the offer of job-based coverage is not "affordable" or not of "minimum value." If either exception is met, an individual is ineligible for minimum essential coverage, making them eligible for premium tax credits.

An employee needs to do this simple test with individual plans less expensive than most group health plans, even without subsidies. With federal and NJ subsidies, the monthly savings are larger than the average car payment.

The "Family Glitch Fix" allows employees with dependent group health coverage to save thousands. Once notified, the fix allows employee dependents denied access to subsidized individual health plans to enroll immediately.

Call us, and we can check affordability in seconds, then calculate your monthly savings in any health plan offered in your area. If your employer offers group health insurance and you have dependents, you may be able to lower your premium costs and their out-of-pocket costs for medical care.

The so-called "family glitch" stems from a 2013 IRS interpretation. Under Section 36B of the Internal Revenue Code, individuals generally do not qualify for premium tax credits if they are eligible for another source of minimum essential coverage, including employer-sponsored plans. There are two exceptions to this rule under the ACA-when the offer of job-based coverage is not "affordable" or not of "minimum value." If either exception is met, an individual is ineligible for minimum essential coverage, making them eligible for premium tax credits.

An employee needs to do this simple test with individual plans less expensive than most group health plans, even without subsidies. With federal and NJ subsidies, the monthly savings are larger than the average car payment.

The "Family Glitch Fix" allows employees with dependent group health coverage to save thousands. Once notified, the fix allows employee dependents denied access to subsidized individual health plans to enroll immediately.

Call us, and we can check affordability in seconds, then calculate your monthly savings in any health plan offered in your area. If your employer offers group health insurance and you have dependents, you may be able to lower your premium costs and their out-of-pocket costs for medical care.

The so-called "family glitch" stems from a 2013 IRS interpretation. Under Section 36B of the Internal Revenue Code, individuals generally do not qualify for premium tax credits if they are eligible for another source of minimum essential coverage, including employer-sponsored plans. There are two exceptions to this rule under the ACA-when the offer of job-based coverage is not "affordable" or not of "minimum value." If either exception is met, an individual is ineligible for minimum essential coverage, making them eligible for premium tax credits.

An employee needs to do this simple test with individual plans less expensive than most group health plans, even without subsidies. With federal and NJ subsidies, the monthly savings are larger than the average car payment.

What are the best health insurance options for small businesses in 2023

Thursday, February 23, 2023 Craig E Chapin, Pesident

In 2023, inflation is the central talking point, and health insurance premiums and medical costs are increasing. Small employers must look at benefit costs with salary, and supply costs increasing. If a business offers health insurance, there are three options; Level Funding, Fully Insured, and Individual Health Plans.

Level funding is the new option with reduced premiums and more comprehensive provider access for groups with good claims experience. Health questions are asked, and past medical usage is checked for insurance companies to select groups that are likely to have lower claims expenses than the premiums paid. Groups with as few as two employees can enroll, and the final premium rates remain level for the policy year. Level funding is a great place to start if you want to see if your groups can save while still having the option to fall back on guaranteed, fully insured health plans.

Fully insured plans are changing and offer savings by reducing provider access, especially to out-of-state providers. Many plan designs are moving away from copays on brand name prescriptions and shifting higher cost sharing to employees. The fully insured plans are favored by employers, paying the lion's share of premiums and wanting to offer benefits with little employee involvement.

The small group's health market is yielding to the individual health market that offers rich federal and (NJ State) premium subsidies to employees and cost-sharing reductions on out-of-pocket costs. The Family Glitch law allows dependents for employees covered by group insurance to take advantage of individual subsidies if the employee's cost to insure their dependents is unaffordable. In NJ, the state exploits the small group market by taking premiums and funding individuals not covered by group insurance.

The best program depends on the business's unique needs and its employees. All groups should offer health insurance as employees are also crushed by inflation. Employees need expert advice to take advantage of any offer and will be more productive, resulting in lower absenteeism from financial loss.

In 2023, inflation is the central talking point, and health insurance premiums and medical costs are increasing. Small employers must look at benefit costs with salary, and supply costs increasing. If a business offers health insurance, there are three options; Level Funding, Fully Insured, and Individual Health Plans.

Level funding is the new option with reduced premiums and more comprehensive provider access for groups with good claims experience. Health questions are asked, and past medical usage is checked for insurance companies to select groups that are likely to have lower claims expenses than the premiums paid. Groups with as few as two employees can enroll, and the final premium rates remain level for the policy year. Level funding is a great place to start if you want to see if your groups can save while still having the option to fall back on guaranteed, fully insured health plans.

Fully insured plans are changing and offer savings by reducing provider access, especially to out-of-state providers. Many plan designs are moving away from copays on brand name prescriptions and shifting higher cost sharing to employees. The fully insured plans are favored by employers, paying the lion's share of premiums and wanting to offer benefits with little employee involvement.

The small group's health market is yielding to the individual health market that offers rich federal and (NJ State) premium subsidies to employees and cost-sharing reductions on out-of-pocket costs. The Family Glitch law allows dependents for employees covered by group insurance to take advantage of individual subsidies if the employee's cost to insure their dependents is unaffordable. In NJ, the state exploits the small group market by taking premiums and funding individuals not covered by group insurance.

The best program depends on the business's unique needs and its employees. All groups should offer health insurance as employees are also crushed by inflation. Employees need expert advice to take advantage of any offer and will be more productive, resulting in lower absenteeism from financial loss.

In 2023, inflation is the central talking point, and health insurance premiums and medical costs are increasing. Small employers must look at benefit costs with salary, and supply costs increasing. If a business offers health insurance, there are three options; Level Funding, Fully Insured, and Individual Health Plans.

Level funding is the new option with reduced premiums and more comprehensive provider access for groups with good claims experience. Health questions are asked, and past medical usage is checked for insurance companies to select groups that are likely to have lower claims expenses than the premiums paid. Groups with as few as two employees can enroll, and the final premium rates remain level for the policy year. Level funding is a great place to start if you want to see if your groups can save while still having the option to fall back on guaranteed, fully insured health plans.

Fully insured plans are changing and offer savings by reducing provider access, especially to out-of-state providers. Many plan designs are moving away from copays on brand name prescriptions and shifting higher cost sharing to employees. The fully insured plans are favored by employers, paying the lion's share of premiums and wanting to offer benefits with little employee involvement.

The small group's health market is yielding to the individual health market that offers rich federal and (NJ State) premium subsidies to employees and cost-sharing reductions on out-of-pocket costs. The Family Glitch law allows dependents for employees covered by group insurance to take advantage of individual subsidies if the employee's cost to insure their dependents is unaffordable. In NJ, the state exploits the small group market by taking premiums and funding individuals not covered by group insurance.

The best program depends on the business's unique needs and its employees. All groups should offer health insurance as employees are also crushed by inflation. Employees need expert advice to take advantage of any offer and will be more productive, resulting in lower absenteeism from financial loss.

The Inflation Reduction Act is welcome news for individual health participants.

Wednesday, August 24, 2022 Craig E. Chapin

The Inflation Reduction act guarantees funding to ACA individual insurance market for the next three years with the enhancements implemented by the American Rescue Law of 2021. Premium subsidies are increased for a household earning less than 400% of the Federal Poverty Level (FPL). The "Income Cliff" has been eliminated, limiting costs to homes at any income to 8.5% if not offered group insurance, based on the second lowest silver level plan in their zip code. The "Family Glitch" is removed, limiting a family's cost to 9.12% of household income even when offered group health insurance through work.

Many small employers will embrace the change allowing low-income employees to take advantage of subsidies while continuing to fund health premiums for higher-paid employees that do not qualify for subsidies. An ICHRA will enable employers to set up a special enrollment event to transition employees from group to individual plans.

A families premium cost as a percentage of the federal poverty level

The Inflation Reduction act guarantees funding to ACA individual insurance market for the next three years with the enhancements implemented by the American Rescue Law of 2021. Premium subsidies are increased for a household earning less than 400% of the Federal Poverty Level (FPL). The "Income Cliff" has been eliminated, limiting costs to homes at any income to 8.5% if not offered group insurance, based on the second lowest silver level plan in their zip code. The "Family Glitch" is removed, limiting a family's cost to 9.12% of household income even when offered group health insurance through work.

Many small employers will embrace the change allowing low-income employees to take advantage of subsidies while continuing to fund health premiums for higher-paid employees that do not qualify for subsidies. An ICHRA will enable employers to set up a special enrollment event to transition employees from group to individual plans.

A families premium cost as a percentage of the federal poverty level

The Inflation Reduction act guarantees funding to ACA individual insurance market for the next three years with the enhancements implemented by the American Rescue Law of 2021. Premium subsidies are increased for a household earning less than 400% of the Federal Poverty Level (FPL). The "Income Cliff" has been eliminated, limiting costs to homes at any income to 8.5% if not offered group insurance, based on the second lowest silver level plan in their zip code. The "Family Glitch" is removed, limiting a family's cost to 9.12% of household income even when offered group health insurance through work.

Many small employers will embrace the change allowing low-income employees to take advantage of subsidies while continuing to fund health premiums for higher-paid employees that do not qualify for subsidies. An ICHRA will enable employers to set up a special enrollment event to transition employees from group to individual plans.

A families premium cost as a percentage of the federal poverty level

- 100% to 133%: Zero Premium Plus Cost Sharing Reductions (CSR)

- 133% to 159%: Zero Premium Plus CSR

- 150% to 200%: Zero to 2% Plus CRS

- 200% to 250%: 2% to 4% Plus CRS

- 250% to 300%: 4% to 6%

- 300% to 300%: 6% to 8.5%

- Over 400%: 8.5%

Offering an ICHRA allows families to elect subsidized Health Plans

Tuesday, October 03, 2021

ICHRA is an employer-funded health benefit that is used to reimburse employees for individual health insurance premiums and healthcare expenses. This exciting benefit gives employers a practical option that creates flexibility and maintains employee satisfaction.

Why is ICHRA such a big deal?

Employers can reimburse employees that do not qualify for Federal subsidies given by the Affordable Care Act and enhanced by the American Rescue Law. With proper plan design, most employees will elect the subsidies for their entire family, so the employer contributes nothing. There are no participation requirements or minimum employer contributions that are part of any group plans. Lastly, the ICHRA allows for a special enrollment event so employers can start a plan any time of the year.

Employee Classes Defined

The ICHRA comes with 11 different employee classes businesses can leverage while structuring benefit eligibility and allowance amounts. The classes separate employees into groups by job-based criteria that include locations, tenure, hours worked, and more. The 11 classes are as follows:

ICHRA is an employer-funded health benefit that is used to reimburse employees for individual health insurance premiums and healthcare expenses. This exciting benefit gives employers a practical option that creates flexibility and maintains employee satisfaction.

Why is ICHRA such a big deal?

Employers can reimburse employees that do not qualify for Federal subsidies given by the Affordable Care Act and enhanced by the American Rescue Law. With proper plan design, most employees will elect the subsidies for their entire family, so the employer contributes nothing. There are no participation requirements or minimum employer contributions that are part of any group plans. Lastly, the ICHRA allows for a special enrollment event so employers can start a plan any time of the year.

Employee Classes Defined

The ICHRA comes with 11 different employee classes businesses can leverage while structuring benefit eligibility and allowance amounts. The classes separate employees into groups by job-based criteria that include locations, tenure, hours worked, and more. The 11 classes are as follows:

- Full-time employees

- Part-time employees

- Salaried employees

- Hourly employees

- Temporary employees of staffing firms

- Seasonal employees

- Employees covered under a collective bargaining agreement

- Employees in a waiting period

- Foreign employees who work abroad

- Employees in different locations, based on rating areas

- A combination of two or more of the above

- 10 employees for employers with fewer than 100 employees

- 10 percent of the total number of employees for employers with between 100 and 200 employees

- 20 employees for employers with more than 200 employees

The ICHRA law gives groups more flexibility.

Friday, October 1, 2021 Craig Chapin

The ICHRA law allows a large employer to meet ACA mandated premiums contributions while not excluding an employee's dependents from taking advantage of individual subsides. The law gives small groups a special enrollment event to offer more choice to employees and voluntary options for individual health subsidies.

In March 2021, The American Rescue law increased federal subsidies to lower the premiums for individuals not offered group health insurance at work. The law also eliminated the income cliff that restricted premium subsidies for anyone earning over 400% of the Federal Poverty Level. Now any qualified individual will not pay more than 8.5% of their household income for their entire family, and most will pay much less. Many groups want to offer employees savings but are not aware of the rules.

The ICHRA law starts a special enrollment event to enroll employees into individual plans at any time of the year. The law allows employers to contribute to their employee's costs and also contribute to their out-of-pocket costs. Employers can offer employees more choice of plans, better network access, and their dependents have full access to health plans with federal and state subsidies to lower their costs. Employers can use classes to segment their employees with different benefits to accommodate management, out-of-state employees, hourly, seasonal, etc., offering employees lower prices and better network access.

Every group needs to take the time to learn the benefits and rules, and individuals pay on average $10 a month using individual plans verse group premiums of $300 or more.

The ICHRA law allows a large employer to meet ACA mandated premiums contributions while not excluding an employee's dependents from taking advantage of individual subsides. The law gives small groups a special enrollment event to offer more choice to employees and voluntary options for individual health subsidies.

In March 2021, The American Rescue law increased federal subsidies to lower the premiums for individuals not offered group health insurance at work. The law also eliminated the income cliff that restricted premium subsidies for anyone earning over 400% of the Federal Poverty Level. Now any qualified individual will not pay more than 8.5% of their household income for their entire family, and most will pay much less. Many groups want to offer employees savings but are not aware of the rules.

The ICHRA law starts a special enrollment event to enroll employees into individual plans at any time of the year. The law allows employers to contribute to their employee's costs and also contribute to their out-of-pocket costs. Employers can offer employees more choice of plans, better network access, and their dependents have full access to health plans with federal and state subsidies to lower their costs. Employers can use classes to segment their employees with different benefits to accommodate management, out-of-state employees, hourly, seasonal, etc., offering employees lower prices and better network access.

Every group needs to take the time to learn the benefits and rules, and individuals pay on average $10 a month using individual plans verse group premiums of $300 or more.

The ICHRA law allows a large employer to meet ACA mandated premiums contributions while not excluding an employee's dependents from taking advantage of individual subsides. The law gives small groups a special enrollment event to offer more choice to employees and voluntary options for individual health subsidies.

In March 2021, The American Rescue law increased federal subsidies to lower the premiums for individuals not offered group health insurance at work. The law also eliminated the income cliff that restricted premium subsidies for anyone earning over 400% of the Federal Poverty Level. Now any qualified individual will not pay more than 8.5% of their household income for their entire family, and most will pay much less. Many groups want to offer employees savings but are not aware of the rules.

The ICHRA law starts a special enrollment event to enroll employees into individual plans at any time of the year. The law allows employers to contribute to their employee's costs and also contribute to their out-of-pocket costs. Employers can offer employees more choice of plans, better network access, and their dependents have full access to health plans with federal and state subsidies to lower their costs. Employers can use classes to segment their employees with different benefits to accommodate management, out-of-state employees, hourly, seasonal, etc., offering employees lower prices and better network access.

Every group needs to take the time to learn the benefits and rules, and individuals pay on average $10 a month using individual plans verse group premiums of $300 or more.

Would you prefer to pay $50 or $500 a month?

Tuesday, May 18, 2021 Craig Chapin

New Jersey residents "Not" offered group health insurance through work save even more with state subsidies in addition to improved Federal subsidies. Many bronze-level individual plans have zero premiums. Family premiums can be less than single plans. Families are also given more choice, with each family member able to pick a different network or plan design. The Affordable Care Act income cliff has been removed, and all eligible households never pay more than 8.5% of their household income, and most pay far less. Everyone in NJ needs to learn their cost at https://enroll.getcovered.nj.gov/hix/preeligibility#/ and notify their employer.

Similar to the Advance Premium Tax Credit (APTC), New Jersey residents will qualify for new savings based on income. Households with annual incomes up to 600% of the FPL will receive the new and expanded NJHPS. An individual with an income of up to $76,560 and a family of four who makes up to $157,200 can receive state subsidies to lower health coverage costs. Anyone who qualifies will be able to see a lower premium when using our plan comparison tool or after filling out an application.

If your employer offers you group health, ask them to learn the detail as they would better serve your interests to cancel the group health and compensate you with better benefits and services.

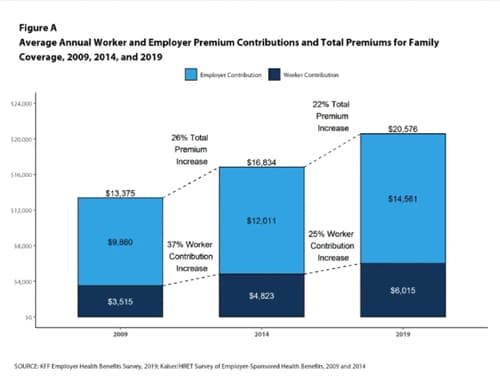

According to the Kaiser Foundation, Independent study in 2019, employers pay 82% of an average $7,188 single premium and 70% of a $20,576 family premium. With these new subsidies, an entire family's health insurance can be less than the 18% an employer asks employees to pay. Most single employees would rather pay $51 a month versus $100 at work, especially if their employer used the employer's premium savings to give more benefits.

Small employers should establish a competitive edge against the competition, utilizing open enrollment during the summer to educate employees on the change and implement new benefits and services. Don't waste thousands in savings waiting for your group renewal or look to change when so many others renew year-end. Your employees are learning the truth as GetCoveredNJ bombards residents on the news. Be the first to take off your mask with the law in place and the government's permission to proceed.

Employers can take the average $6,000 in employer-paid premium savings and give every employee a defined contribution to purchase benefits and services they want. Don't follow the pack and wait for others to take the lead. Tell your employer to act now as waiting for everyone to take off their mask and following the pack can cost you thousands.

New Jersey residents "Not" offered group health insurance through work save even more with state subsidies in addition to improved Federal subsidies. Many bronze-level individual plans have zero premiums. Family premiums can be less than single plans. Families are also given more choice, with each family member able to pick a different network or plan design. The Affordable Care Act income cliff has been removed, and all eligible households never pay more than 8.5% of their household income, and most pay far less. Everyone in NJ needs to learn their cost at https://enroll.getcovered.nj.gov/hix/preeligibility#/ and notify their employer.

Similar to the Advance Premium Tax Credit (APTC), New Jersey residents will qualify for new savings based on income. Households with annual incomes up to 600% of the FPL will receive the new and expanded NJHPS. An individual with an income of up to $76,560 and a family of four who makes up to $157,200 can receive state subsidies to lower health coverage costs. Anyone who qualifies will be able to see a lower premium when using our plan comparison tool or after filling out an application.

If your employer offers you group health, ask them to learn the detail as they would better serve your interests to cancel the group health and compensate you with better benefits and services.

According to the Kaiser Foundation, Independent study in 2019, employers pay 82% of an average $7,188 single premium and 70% of a $20,576 family premium. With these new subsidies, an entire family's health insurance can be less than the 18% an employer asks employees to pay. Most single employees would rather pay $51 a month versus $100 at work, especially if their employer used the employer's premium savings to give more benefits.

Small employers should establish a competitive edge against the competition, utilizing open enrollment during the summer to educate employees on the change and implement new benefits and services. Don't waste thousands in savings waiting for your group renewal or look to change when so many others renew year-end. Your employees are learning the truth as GetCoveredNJ bombards residents on the news. Be the first to take off your mask with the law in place and the government's permission to proceed.

Employers can take the average $6,000 in employer-paid premium savings and give every employee a defined contribution to purchase benefits and services they want. Don't follow the pack and wait for others to take the lead. Tell your employer to act now as waiting for everyone to take off their mask and following the pack can cost you thousands.

New Jersey residents "Not" offered group health insurance through work save even more with state subsidies in addition to improved Federal subsidies. Many bronze-level individual plans have zero premiums. Family premiums can be less than single plans. Families are also given more choice, with each family member able to pick a different network or plan design. The Affordable Care Act income cliff has been removed, and all eligible households never pay more than 8.5% of their household income, and most pay far less. Everyone in NJ needs to learn their cost at https://enroll.getcovered.nj.gov/hix/preeligibility#/ and notify their employer.

Similar to the Advance Premium Tax Credit (APTC), New Jersey residents will qualify for new savings based on income. Households with annual incomes up to 600% of the FPL will receive the new and expanded NJHPS. An individual with an income of up to $76,560 and a family of four who makes up to $157,200 can receive state subsidies to lower health coverage costs. Anyone who qualifies will be able to see a lower premium when using our plan comparison tool or after filling out an application.

If your employer offers you group health, ask them to learn the detail as they would better serve your interests to cancel the group health and compensate you with better benefits and services.

According to the Kaiser Foundation, Independent study in 2019, employers pay 82% of an average $7,188 single premium and 70% of a $20,576 family premium. With these new subsidies, an entire family's health insurance can be less than the 18% an employer asks employees to pay. Most single employees would rather pay $51 a month versus $100 at work, especially if their employer used the employer's premium savings to give more benefits.

Small employers should establish a competitive edge against the competition, utilizing open enrollment during the summer to educate employees on the change and implement new benefits and services. Don't waste thousands in savings waiting for your group renewal or look to change when so many others renew year-end. Your employees are learning the truth as GetCoveredNJ bombards residents on the news. Be the first to take off your mask with the law in place and the government's permission to proceed.

Employers can take the average $6,000 in employer-paid premium savings and give every employee a defined contribution to purchase benefits and services they want. Don't follow the pack and wait for others to take the lead. Tell your employer to act now as waiting for everyone to take off their mask and following the pack can cost you thousands.

Give employees more Financial and Wellness protection with Government funding

Thursday, May 1, 2021 Craig E. Chapin

If you learned, you could pay $500 or $100 for your employee's same health insurance plan. What would you do? Would you give me 15 minutes? Communicating with employers in the post-COVID-19 economy is difficult as remote workers use phone mail and emails as the first line of communication. Employees tell your employers. Owners call now.

Many employers paying for small group health insurance are doing their employees a disservice. However, they are stuck believing there is no better way or don't have the facts. Employee compensation comes in many forms, and with proper education, your employees will cherish the change. While the government pays 75% of any family's health insurance premiums not offered group health insurance, your company paying for group health insurance is obsolete.

Our program is not a trick, but individuals not offered group health insurance get this deal, and we are exploiting it. Don't fight the Fed. Use the premiums savings to compensate employees for other valuable benefits and services. Consider paying your employees differently. They will not disapprove if you give them the money you currently contribute for their group health insurance. Employees will appreciate the change with proper education, especially if you use our system to legally take the money from their pay and automatically pay their insurance premiums each month.

We have a seamless system to transition employees from group health to individual subsidized health insurance. Your company can take credit for giving a defined contribution to employees to pay out-of-pocket medical and dental costs, pay off student loans, child care cost, or save funds in a Health Savings Account.

To utilize these savings, small employers must give up the offer of health insurance, with the compliance obligations on participation, contributions, and continuation. Compensation comes in many forms but raising pay to cover subsided individual plans is not allowed under the Affordable Care Act. However, using a defined contribution for employees to purchase other benefits and services is legal. As a brokerage firm, we can work one-on-one with your employees to enroll families with any carrier in any individual plans. At the same time, our firm can use our traditional group product education and a paperless enrollment system to accumulate employee demographics and educate and enroll employees on any number of benefits and services 24/7 using their smartphones.

A February study shows over 60% of small groups replaced their broker last year for brokers that identified ways to drive down costs and offer better service. Offering non-traditional benefits and increasing productivity by handing over the reins to our technology platform can help your company achieve greater efficiency and allow your company to merge data with payroll and HR administration.

The Post-COVID-19 economy has changed for good. The new administration wants socialized insurance and will pay to get it. Don't try to compete with the Fed but take advantage of the savings. Use our service to simplify the transition while expanding your employee's financial and wellness protection. Productivity will excel, and recruitment and retention will increase.

If you learned, you could pay $500 or $100 for your employee's same health insurance plan. What would you do? Would you give me 15 minutes? Communicating with employers in the post-COVID-19 economy is difficult as remote workers use phone mail and emails as the first line of communication. Employees tell your employers. Owners call now.

Many employers paying for small group health insurance are doing their employees a disservice. However, they are stuck believing there is no better way or don't have the facts. Employee compensation comes in many forms, and with proper education, your employees will cherish the change. While the government pays 75% of any family's health insurance premiums not offered group health insurance, your company paying for group health insurance is obsolete.

Our program is not a trick, but individuals not offered group health insurance get this deal, and we are exploiting it. Don't fight the Fed. Use the premiums savings to compensate employees for other valuable benefits and services. Consider paying your employees differently. They will not disapprove if you give them the money you currently contribute for their group health insurance. Employees will appreciate the change with proper education, especially if you use our system to legally take the money from their pay and automatically pay their insurance premiums each month.

We have a seamless system to transition employees from group health to individual subsidized health insurance. Your company can take credit for giving a defined contribution to employees to pay out-of-pocket medical and dental costs, pay off student loans, child care cost, or save funds in a Health Savings Account.

To utilize these savings, small employers must give up the offer of health insurance, with the compliance obligations on participation, contributions, and continuation. Compensation comes in many forms but raising pay to cover subsided individual plans is not allowed under the Affordable Care Act. However, using a defined contribution for employees to purchase other benefits and services is legal. As a brokerage firm, we can work one-on-one with your employees to enroll families with any carrier in any individual plans. At the same time, our firm can use our traditional group product education and a paperless enrollment system to accumulate employee demographics and educate and enroll employees on any number of benefits and services 24/7 using their smartphones.

A February study shows over 60% of small groups replaced their broker last year for brokers that identified ways to drive down costs and offer better service. Offering non-traditional benefits and increasing productivity by handing over the reins to our technology platform can help your company achieve greater efficiency and allow your company to merge data with payroll and HR administration.

The Post-COVID-19 economy has changed for good. The new administration wants socialized insurance and will pay to get it. Don't try to compete with the Fed but take advantage of the savings. Use our service to simplify the transition while expanding your employee's financial and wellness protection. Productivity will excel, and recruitment and retention will increase.

If you learned, you could pay $500 or $100 for your employee's same health insurance plan. What would you do? Would you give me 15 minutes? Communicating with employers in the post-COVID-19 economy is difficult as remote workers use phone mail and emails as the first line of communication. Employees tell your employers. Owners call now.

Many employers paying for small group health insurance are doing their employees a disservice. However, they are stuck believing there is no better way or don't have the facts. Employee compensation comes in many forms, and with proper education, your employees will cherish the change. While the government pays 75% of any family's health insurance premiums not offered group health insurance, your company paying for group health insurance is obsolete.

Our program is not a trick, but individuals not offered group health insurance get this deal, and we are exploiting it. Don't fight the Fed. Use the premiums savings to compensate employees for other valuable benefits and services. Consider paying your employees differently. They will not disapprove if you give them the money you currently contribute for their group health insurance. Employees will appreciate the change with proper education, especially if you use our system to legally take the money from their pay and automatically pay their insurance premiums each month.

We have a seamless system to transition employees from group health to individual subsidized health insurance. Your company can take credit for giving a defined contribution to employees to pay out-of-pocket medical and dental costs, pay off student loans, child care cost, or save funds in a Health Savings Account.

To utilize these savings, small employers must give up the offer of health insurance, with the compliance obligations on participation, contributions, and continuation. Compensation comes in many forms but raising pay to cover subsided individual plans is not allowed under the Affordable Care Act. However, using a defined contribution for employees to purchase other benefits and services is legal. As a brokerage firm, we can work one-on-one with your employees to enroll families with any carrier in any individual plans. At the same time, our firm can use our traditional group product education and a paperless enrollment system to accumulate employee demographics and educate and enroll employees on any number of benefits and services 24/7 using their smartphones.

A February study shows over 60% of small groups replaced their broker last year for brokers that identified ways to drive down costs and offer better service. Offering non-traditional benefits and increasing productivity by handing over the reins to our technology platform can help your company achieve greater efficiency and allow your company to merge data with payroll and HR administration.

The Post-COVID-19 economy has changed for good. The new administration wants socialized insurance and will pay to get it. Don't try to compete with the Fed but take advantage of the savings. Use our service to simplify the transition while expanding your employee's financial and wellness protection. Productivity will excel, and recruitment and retention will increase.

The American Rescue Plan Makes Group Health Obsolete

Monday, March 11, 2021 Craig E. Chapin

The American Rescue Bill was signed into law on March 11, 2021, vastly changing individual health coverage subsidies. The new subsidies are fully funded for two years, but we feel this new entitlement will be continued at least while President Biden is in office. He ran on fixing Obamacare, and this is the first step.

Planned or not, the savings are so significant that employers should consider canceling their group health plans and compensating their employees with the premium saving. An employer can eliminate complying with COBRA, and Family leaves laws. Employees would have a wider choice on plan design, dependents would not be cut out from subsidies, and employers would not have to comply with minimum premium contributions or participation requirements.

The list of enhanced supplements and tax savings vehicles is broad and just another form of compensation. Some employees would benefit from first dollar benefits funding into a flexible spending account or health savings account. Others may want an accident, dental, disability, cancer, critical illness, life, long-term care, and vision insurance. Students may wish to pay off their student loans or want more reimbursements for remote offices, including cell phone and internet costs. All of these benefits can be offered on an employer or employee-paid basis.

We have a system to educate workers and transition them to individual plans. Our program allows an employer to offer an online platform offering a complete package of customized services and supplemental plans.

Studies show that employees desire benefits second to compensation. A more comprehensive choice of services gives small employers the upper hand when recruiting new help and retaining valued workers. Don't try to complete with Federal subsidies and use the savings to provide more first dollar benefits to your employees. Entitlement programs may change but generally never disappear.

The American Rescue Bill was signed into law on March 11, 2021, vastly changing individual health coverage subsidies. The new subsidies are fully funded for two years, but we feel this new entitlement will be continued at least while President Biden is in office. He ran on fixing Obamacare, and this is the first step.

Planned or not, the savings are so significant that employers should consider canceling their group health plans and compensating their employees with the premium saving. An employer can eliminate complying with COBRA, and Family leaves laws. Employees would have a wider choice on plan design, dependents would not be cut out from subsidies, and employers would not have to comply with minimum premium contributions or participation requirements.

The list of enhanced supplements and tax savings vehicles is broad and just another form of compensation. Some employees would benefit from first dollar benefits funding into a flexible spending account or health savings account. Others may want an accident, dental, disability, cancer, critical illness, life, long-term care, and vision insurance. Students may wish to pay off their student loans or want more reimbursements for remote offices, including cell phone and internet costs. All of these benefits can be offered on an employer or employee-paid basis.

We have a system to educate workers and transition them to individual plans. Our program allows an employer to offer an online platform offering a complete package of customized services and supplemental plans.

Studies show that employees desire benefits second to compensation. A more comprehensive choice of services gives small employers the upper hand when recruiting new help and retaining valued workers. Don't try to complete with Federal subsidies and use the savings to provide more first dollar benefits to your employees. Entitlement programs may change but generally never disappear.

The American Rescue Bill was signed into law on March 11, 2021, vastly changing individual health coverage subsidies. The new subsidies are fully funded for two years, but we feel this new entitlement will be continued at least while President Biden is in office. He ran on fixing Obamacare, and this is the first step.

Planned or not, the savings are so significant that employers should consider canceling their group health plans and compensating their employees with the premium saving. An employer can eliminate complying with COBRA, and Family leaves laws. Employees would have a wider choice on plan design, dependents would not be cut out from subsidies, and employers would not have to comply with minimum premium contributions or participation requirements.